Research Note: Vertical (dis)Integration in Music

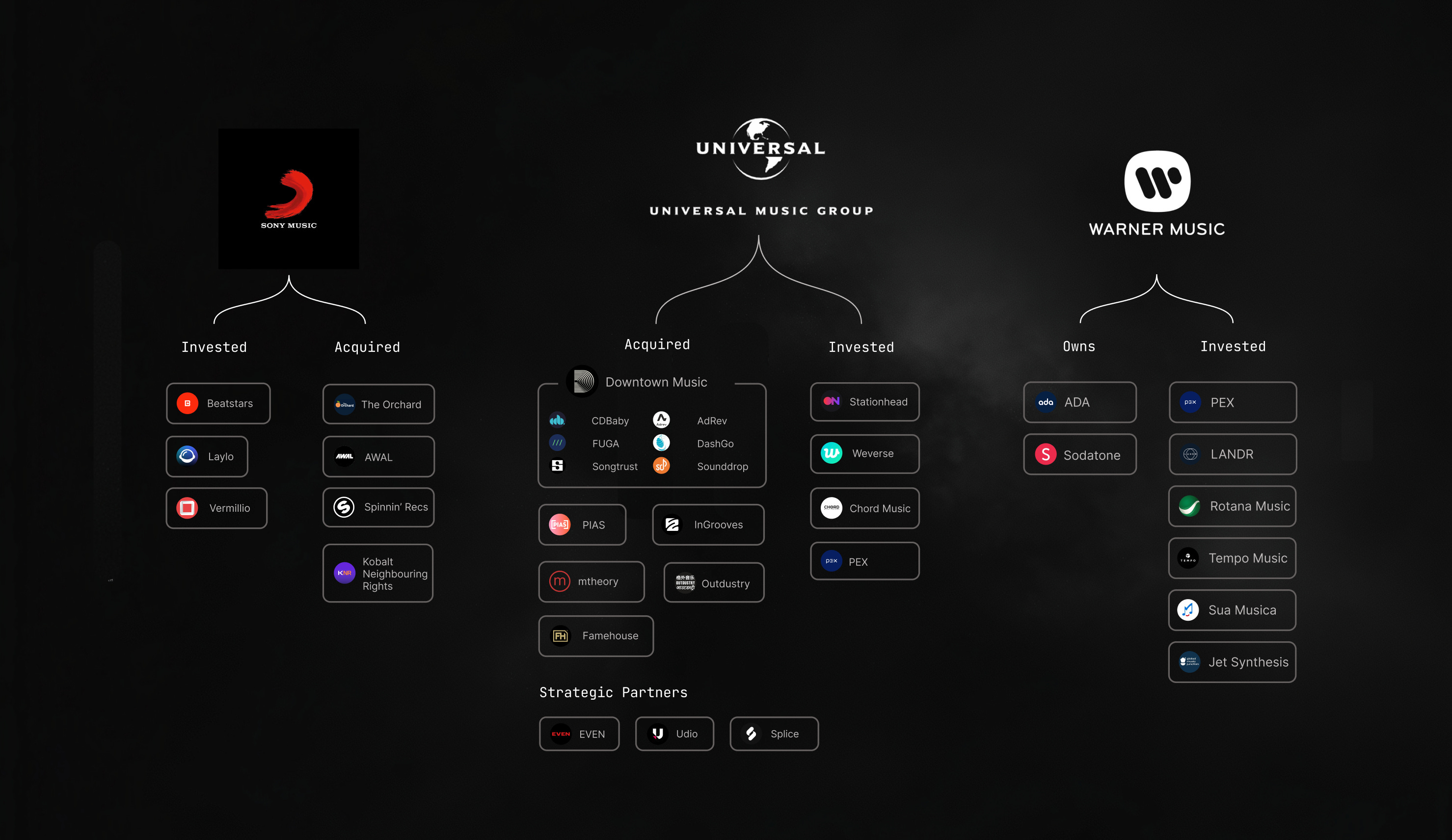

musicben just published a very cool data-visual over on his STVDIO+ newsletter, where he pulled together a small database of recent acquisitions and investments made by the big three major record labels.1

As you can see, the majors have been on a buying spree in recent times. Alongside the map, Ben convincingly argues that a substantial share of this investment is concentrated in distribution and related infrastructure, reflecting a major label strategy to secure greater leverage over DSPs and exert more control over the “highway” through which independent music reaches audiences. He further suggests that this positioning matters even more in an AI-driven future, where control over catalog access, attribution systems, and payment rails may become increasingly strategic. As Ben writes, “It’s a worrying trend that leaves fewer and fewer independent paths to releasing music.”

What Ben is documenting is a form of horizontal integration, where each major is expanding its ownership of complementary businesses operating at roughly the same point in the value chain. All three majors now hold multiple independent music distribution-related businesses, providing control over an increasingly important layer of the pipeline through which independent music is delivered to platforms, monetized, and brought to market. That, in turn, gives them not only another source of revenue, but also greater strategic leverage over a part of the ecosystem that more and more artists now rely on.

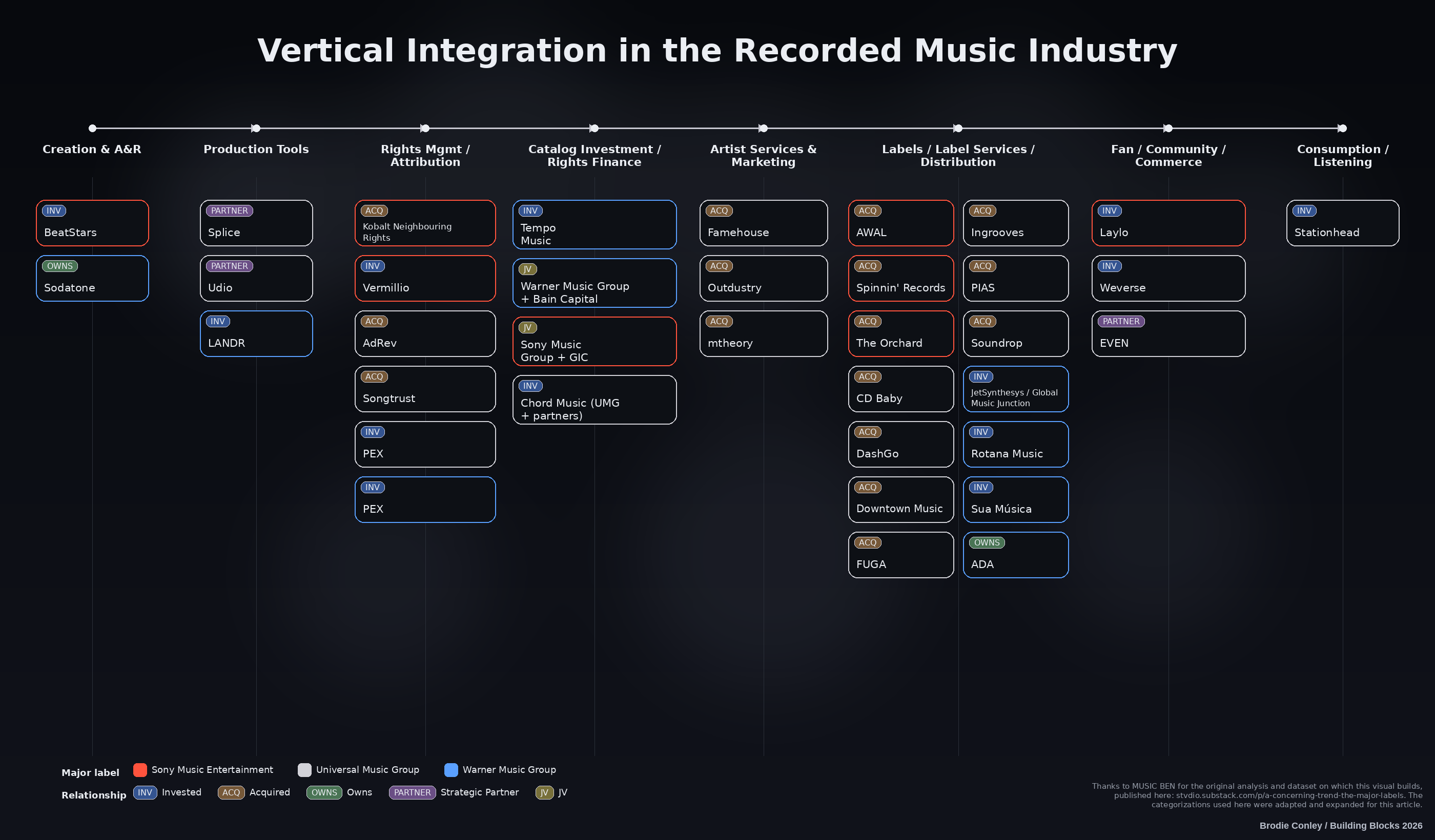

When I saw Ben’s graphic, it struck me that it could be useful to add another layer of categorization by locating each acquisition and investment within the broader music value chain:

To do that, I divided the music value chain into eight constituent categories and then classified each deal highlighted by Ben accordingly23: (1) Creation & A&R; (2) Production Tools; (3) Rights Management / Attribution; (4) Catalog Investment / Rights Finance; (5) Artist Services & Marketing; (6) Labels / Label Services / Distribution; (7) Fan / Community / Commerce; and (8) Consumption / Listening.

Even a quick glance at the map shows that, while there are clearly some parts of the value chain attracting heavier investment (like distribution, as Ben notes), the majors’ acquisitions and stakes are spread across nearly the entire chain, from creation to consumption.

This is vertical integration, where companies attempt to own or control multiple stages of the supply and value chain. This is not new to those of us who have been paying attention to the music industry recently, as indies assembled a broad coalition to oppose Virgin Music’s acquisition of Downtown on competition grounds, including vertical integration concerns.

While there is nothing especially novel about pointing to vertical integration as a problem in music, investment maps like this still serve a useful purpose. They make visible how the major music companies are deploying capital through investment to consolidate control across the full value chain, and with it their power to shape the terms on which artists, workers, and smaller firms operate.

These are not speculative risks; they are well-recognized competition concerns across the United States, the European Union, and Canada.4 We know that vertical integration can, for example:

Produce foreclosure, cutting rivals off from key inputs, services, datasets, or routes to market (e.g., an independent artist or label losing access to a key distribution or playlisting channel.)

Enable self-preferencing, allowing integrated firms to favour their own repertoire and affiliated services over independents (e.g., a platform giving better placement to music tied to its own label group, or in which a label group has equity stakes.).

Increase bargaining leverage by bundling multiple services across the chain into offers that artists and smaller firms may have reduced ability to refuse (e.g., offering distribution, marketing, and advances as one package.).

Concentrate data and attribution power, giving a handful of firms greater control over the metadata, listener information, and recommendation systems that increasingly determine visibility and payment (e.g., controlling the financial, accounting, metadata and recommendation systems that determine visibility and royalties).

Facilitate cross-subsidization, allowing dominant firms to use profits from one line of business to underprice competitors in another (e.g., using profits from a major catalog to underprice an affiliated marketing or label-services arm.).

Although the European Commission ultimately approved the Downtown transaction, the campaign was not for nought. As a condition of approval, Downtown was required to divest Curve Royalty Systems, a platform central to the financial operations of many independent music companies. That is why, fortunately, Curve does not appear in this map.

This demonstrates that even where regulators approve a transaction, coordinated opposition can still shape the outcome, narrow the scope of a deal, and clarify the stakes for the wider sector. In this case, the requirement that Downtown divest Curve was not a trivial concession. It reduced one of the clearest risks of the integration by helping prevent sensitive financial data from independent music companies using Curve from flowing into major-label hands, where it could have been used to deepen their informational advantage and bargaining power.

Ultimately, what investment maps like these make clear is that the issue is not just one of individual acquisitions or isolated markets. There is a broader pattern of consolidation and integration — both horizontal and vertical — across music, through which the majors and other large holders of capital are deepening their power over the infrastructure that increasingly determines how music is made, circulated, and paid for. If that trend is to be challenged, artists, workers, and independent firms will need to strengthen their coalition, while pooling resources for the research, policy and regulatory advocacy, public education, and organizing needed to resist it.

Some Music!

Since we’re talking about how vertical integration can lead to the disintegration of the institutions needed for a sustainable music ecosystem, it seems only fitting to turn to William Basinski’s ‘Disintegration Loops’, a dark, haunting record that feels uncomfortably well suited to the present moment.

For anyone interested, here is the Excel file in which I classified each investment:5

Notably, the map also includes Warner’s ownership of ADA, which has been part of WMG since its founding in 1993. Presumably, Ben included ADA to reflect the extent of distribution control held across the big three labels. I have kept it in my own analysis for the same reason.

To be clear, these are ideal types. The value-chain categories aren’t perfectly mutually exclusive, and the linear mapping (left to right) is intended to show a general flow, rather than an exhaustive model. In reality, the recorded music value chain involves substantial overlap and complex interactions across its different parts.

Ben’s original graphic included UMG’s recent catalog investment vehicle, Chord Music, but did not include Sony and GIC’s music catalog investment partnership or Warner Music and Bain Capital’s recent catalog venture. For the sake of consistency, I added both of the latter to my analysis.

See, for example, the US DOJ Merger Guidelines; the European Commission’s Article 102 procedures; and the Government of Canada Merger Enforcement Guidelines. Note, that Canada’s merger guidelines are currently being updated; the Competition Bureau released proposed revised guidelines for public consultation, which just wrapped in early February.

Feel free to DM me if you think I have misclassified anything.

Enjoyed your take on this. Definitely lays it all out there, a transparent display of key player interests.

I do not to see any sync licensing companies in your graph. It seems most of those companies (Songtradr, Chordal etc…) are still overlooked, since most licensing is handled in-house at labels and publishers working on big film and TV campaigns.

For that reason I believe sync licensing provides one of the biggest opportunities the indie community has to generate real disruption from the very bottom of the long tail. 5.2B+ people scroll and there is currently still no efficient system for brands to license real music at scale for social media…

Nice work and good read. Got a question for you - do you think there’s a kind of inevitable push and pull that is fundamentally part of the ecology of startups, innovation and business?

Streaming and Distributions massive shifts largely opened up the value from what I remember it looking like when I was first starting out in music back in 2000. Hell very different than it looked when I left Sony a decade ago… That lead to a lot of innovation.

I wonder if we need to look at this kind of consolidation as a zero sum game in the moment or more like a process - tidal maybe (there’s almost a bad pun buried in there somewhere) and in turn be ready or building for where the new opportunities are.